Synopsis

China now absorbs ~21% of Latin America’s exports (~$180B annually), surpassing the US and EU. Anchored in resources and reinforced by infrastructure, this corridor is structurally redrawing commodity pricing power, supply chains, and geopolitical leverage.

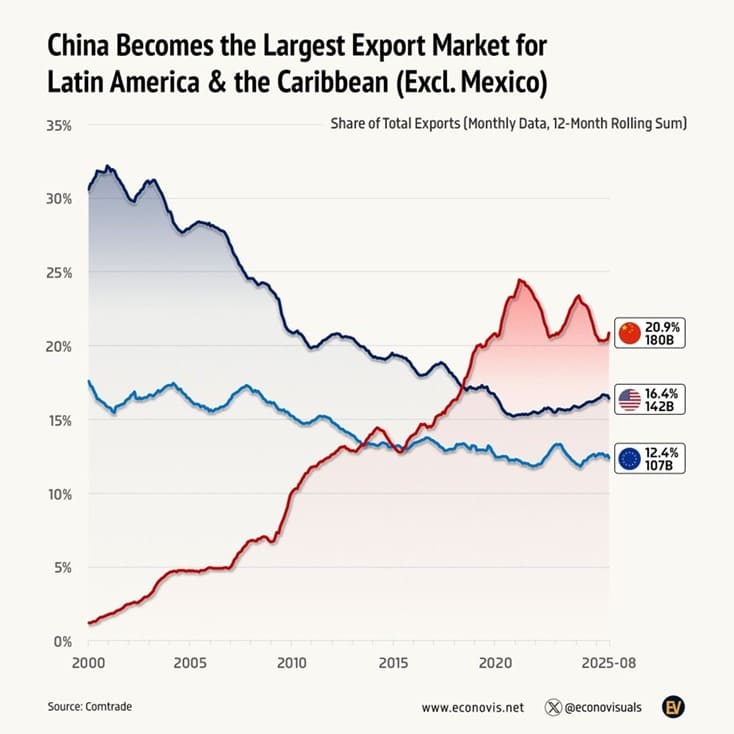

China has quietly become the largest export market for Latin America and the Caribbean (excluding Mexico). As of the latest rolling data, China accounts for roughly 21% of the region’s exports, surpassing the United States (~16%) and the European Union (~12%). In absolute terms, China now imports close to $180 billion worth of goods annually from the region—well ahead of Western economies.

This is not a temporary spike. China’s share has risen steadily for more than two decades, gaining roughly 20 percentage points since 2000, while Western shares have gradually declined. The implication is structural: Latin America is increasingly integrated into China’s economic engine.

Why China Is Winning Latin America’s Export Share

1. Resource Alignment

Latin America produces exactly what China needs to sustain industrial growth and food security—energy, metals, and agricultural commodities. Trade between the two is anchored in raw materials rather than finished goods, making the relationship complementary rather than competitive.

2. Trade Plus Infrastructure Strategy

China’s approach is not limited to buying commodities. It combines trade with financing, logistics investment, and infrastructure development, creating long-term economic linkages. When ports, railways, and supply chains are built around a particular trade partner, that relationship becomes structurally durable.

3. Strategic Diversification by China

Securing commodity supply is a core strategic objective for Beijing. By expanding trade ties with Latin America, China reduces reliance on traditional suppliers and strengthens its influence across resource corridors that are essential to global manufacturing.

What This Means for Global Markets

Commodity pricing becomes more China-centric.

If China remains the dominant marginal buyer of Latin American output, global commodity cycles—from metals to agriculture—will increasingly respond to Chinese growth, policy stimulus, and credit conditions.

Geopolitical competition is shifting regions.

Latin America has historically been closely tied to Western economies. China’s rising share alters bargaining power, trade dynamics, and long-term economic alignment across the region.

Supply chains are being rewritten upstream.

Control over raw materials is as important as control over manufacturing. By deepening trade relationships with resource-rich regions, China is strengthening its influence over the earliest stages of global production chains.

Why This Matters for India

India operates within the same global commodity ecosystem. A stronger China–Latin America trade corridor can influence:

- input costs for global manufacturing

- industrial metal price cycles

- energy inflation dynamics

- currency stability across emerging markets

In practical terms, shifts in this trade axis can affect everything from inflation trajectories to sector profitability across importing economies.

Final Perspective

China’s expanding share of Latin American exports is not a headline trend—it is a structural rebalancing of global trade geography. The relationship is anchored in complementary economic needs, reinforced by infrastructure, and supported by long-term strategic intent.

This tells us something important:

Global power is not only measured by GDP or military strength.

It is measured by who controls the trade corridors that supply the world’s resources.

China is steadily strengthening its position along those corridors.

For investors, the lesson is simple:

Watch trade flows. They often reveal the future long before markets price it.

Disclaimer:

This blog is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any financial instrument. Views expressed are based on publicly available information and market understanding at the time of writing and are subject to change. Readers should consult their financial advisor before making any investment decisions. Investments in markets are subject to risk.