Synopsis

Silver markets show early squeeze signals as China inventories drop ~90%, export controls tighten, and COMEX registered stocks stay thin. With industrial demand firm and relief valves weakening, structural supply stress is building beneath calm prices.

A commodity squeeze rarely begins with headlines. It begins quietly—inventories fall, flows shift, rules tighten, and price stops reacting normally. Silver today is displaying exactly those early signals. Beneath the surface of what appears to be a functioning global market, a structural shift is underway: physical metal is tightening while paper claims remain abundant.

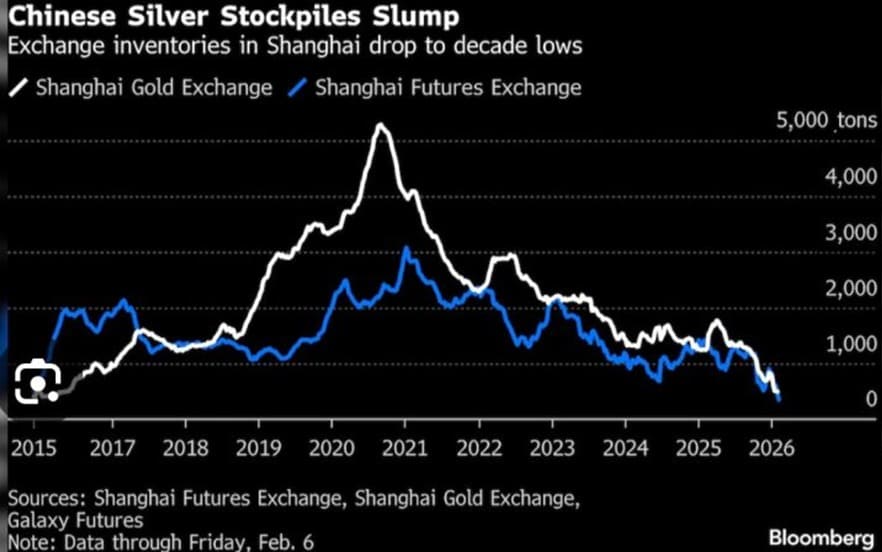

China’s Shrinking Stockpile — The First Warning Signal

The most visible stress indicator is coming from China, one of the world’s largest physical metals hubs.

Key observations:

- Exchange inventories have fallen to ~350 tonnes

- Down nearly 90% from the 2021 peak above 3,000 tonnes

- Represents the lowest level in nearly a decade

This is not a routine cycle fluctuation. Such sharp declines almost always reflect structural supply redistribution, not temporary demand spikes.

The primary driver was a massive export wave in 2025, when hundreds of tonnes of silver were shipped overseas to relieve tightness in global markets. In effect, China acted as a stabilizer for international supply—but doing so drained its own domestic reserves.

Once inventories drop this low, the system becomes fragile. Buffers disappear, and even modest demand increases can trigger market stress.

From Export Engine to Supply Gatekeeper

When a major supplier sees domestic inventories falling sharply, policy response usually follows. That is exactly what is happening now.

Structural policy shift underway:

- China is tightening control over outbound silver flows

- Export permissions are becoming more selective

- Domestic stability is being prioritized over global liquidity

This transition is critical. It signals that China is no longer willing to function as the global pressure-release valve for physical shortages. In commodity cycles, such policy pivots often mark inflection points. They indicate that future shortages may not be resolved as easily as before.

Exchange Rule Changes — The Market’s Quiet Alarm System

Markets rarely announce stress directly. Instead, they reveal it through rule adjustments. When exchanges tighten position rules or hedging permissions, it usually means liquidity conditions are thinner than they appear.

Recent trading framework changes have made it harder for traders to maintain short positions during near-delivery months unless they hold approved hedge exposure.

Why this matters:

- Low inventories increase delivery risk

- Short sellers become structurally vulnerable

- Exchanges reduce leverage to prevent disorderly squeezes

Rule tightening is not random. It is often a sign that exchanges see risks building beneath the surface.

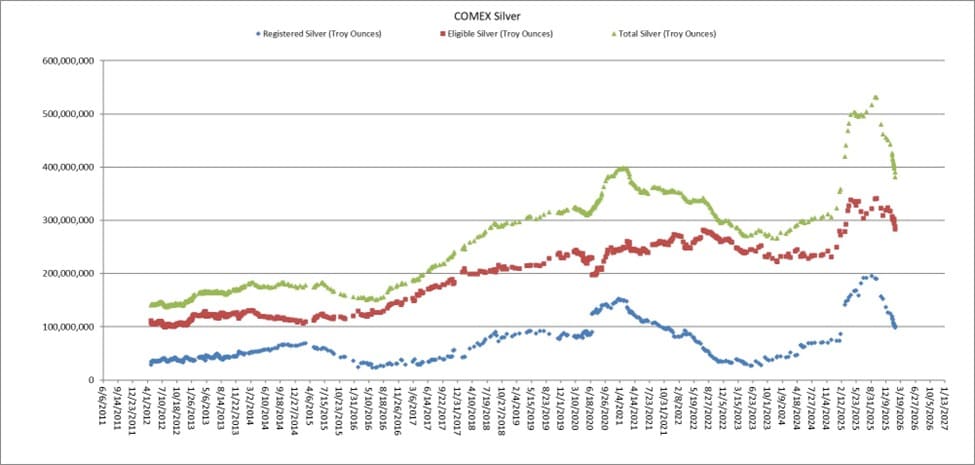

COMEX Inventories — Small Float, Large Market

Another important signal is emerging from global futures markets. Deliverable silver registered for settlement currently sits near ~93 million ounces.

On its own, that number sounds large. In context, it is relatively small.

Why it matters:

- Futures markets rely on the assumption that most contracts are cash-settled

- Only a small fraction normally requests delivery

- When inventories are tight, that assumption becomes fragile

The system works smoothly as long as delivery demand stays low. But when confidence shifts toward physical ownership, even modest increases in delivery requests can stress the structure.

This is why professional commodity traders track registered inventory, not just total stock.

Silver’s Structural Weakness vs Gold

Silver’s supply dynamics are fundamentally different from gold’s.

Gold

- Primarily stored

- Rarely consumed

- Massive above-ground reserves

Silver

- Heavily industrial

- Constantly consumed

- Limited recyclable supply

Industrial sectors such as solar panels, electronics, batteries, and advanced manufacturing remove silver from circulation permanently. Once used, much of it cannot be economically recovered.

This makes silver inherently more sensitive to supply shocks. When demand stays strong and inventories fall, prices don’t need a major catalyst—they only need a marginal imbalance.

When Market Relief Valves Disappear

Historically, commodity squeezes resolve through one of four stabilizers:

- Inventories are released

- Scrap supply increases

- Demand slows

- Metal flows from surplus regions

Right now, several of those stabilizers are weakening simultaneously:

- Inventories are already depleted

- China’s export flexibility is tightening

- Industrial demand remains firm

When multiple relief mechanisms weaken together, markets become extremely sensitive to shocks that would normally be absorbed.

What This Pattern Historically Signals

Commodity history shows that squeezes rarely start with dramatic price spikes. They begin with inventory erosion, policy tightening, and structural demand strength—exactly the combination appearing now.

Silver still looks orderly on the surface. But beneath that calm, conditions resemble the early phases of past commodity repricing cycles.

The Structural Takeaway

This is not yet a crisis. It is a transition.

Key structural signals now visible:

- Physical inventories declining globally

- Export flexibility narrowing

- Exchange rules tightening

- Industrial demand staying strong

Individually, none of these guarantee a squeeze. Together, they form a pattern markets have seen repeatedly before major revaluations.

Markets tend to stay calm until they don’t.

Silver today is moving quietly from a world of abundance assumptions to one of supply reality.

And in commodity markets, reality always sets the price.

Disclaimer:

This blog is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any financial instrument. Views expressed are based on publicly available information and market understanding at the time of writing and are subject to change. Readers should consult their financial advisor before making any investment decisions. Investments in markets are subject to risk.