Synopsis

The 2022 nickel squeeze exposed how leverage and thin liquidity can overpower fundamentals. As short covering met vanishing sellers, prices spiked above $100,000/tonne, forcing the LME to halt trading and cancel trades—revealing structural fragility in commodity markets.

A true story of leverage, geopolitics, and a commodity that ran out of sellers

It began quietly—like most market crises do—not with panic, but with numbers on risk dashboards that looked manageable until suddenly they weren’t.

In early March 2022, nickel markets were already tense. Russia, one of the world’s most important suppliers of high-grade nickel used in batteries and stainless steel, had become the center of global geopolitical uncertainty. Traders began asking the only question that matters in commodity markets:

Will supply arrive?

That uncertainty alone was enough to push prices higher. But what the market didn’t yet fully understand was that one of the world’s largest metals producers—Tsingshan Holding Group, led by Chinese industrialist Xiang Guangda—was sitting on an enormous short position in nickel.

It had been built as a hedge.

It worked—until it didn’t.

Act I — The Hedge That Became a Trap

Short positions are not dangerous when prices fall or move slowly. They become dangerous when prices rise quickly.

As nickel climbed, margin calls began. The system demanded cash collateral immediately. The more prices rose, the more cash was required. The more collateral demanded, the more the short position had to be reduced.

That is when hedging turns into forced buying.

Nickel is not a deep market like global equities. Liquidity is thin, and sellers can vanish during stress. As Tsingshan rushed to cover exposure, prices surged faster, triggering even larger margin calls. The feedback loop had begun.

The market stopped trading fundamentals.

It started trading survival.

Act II — The Explosion

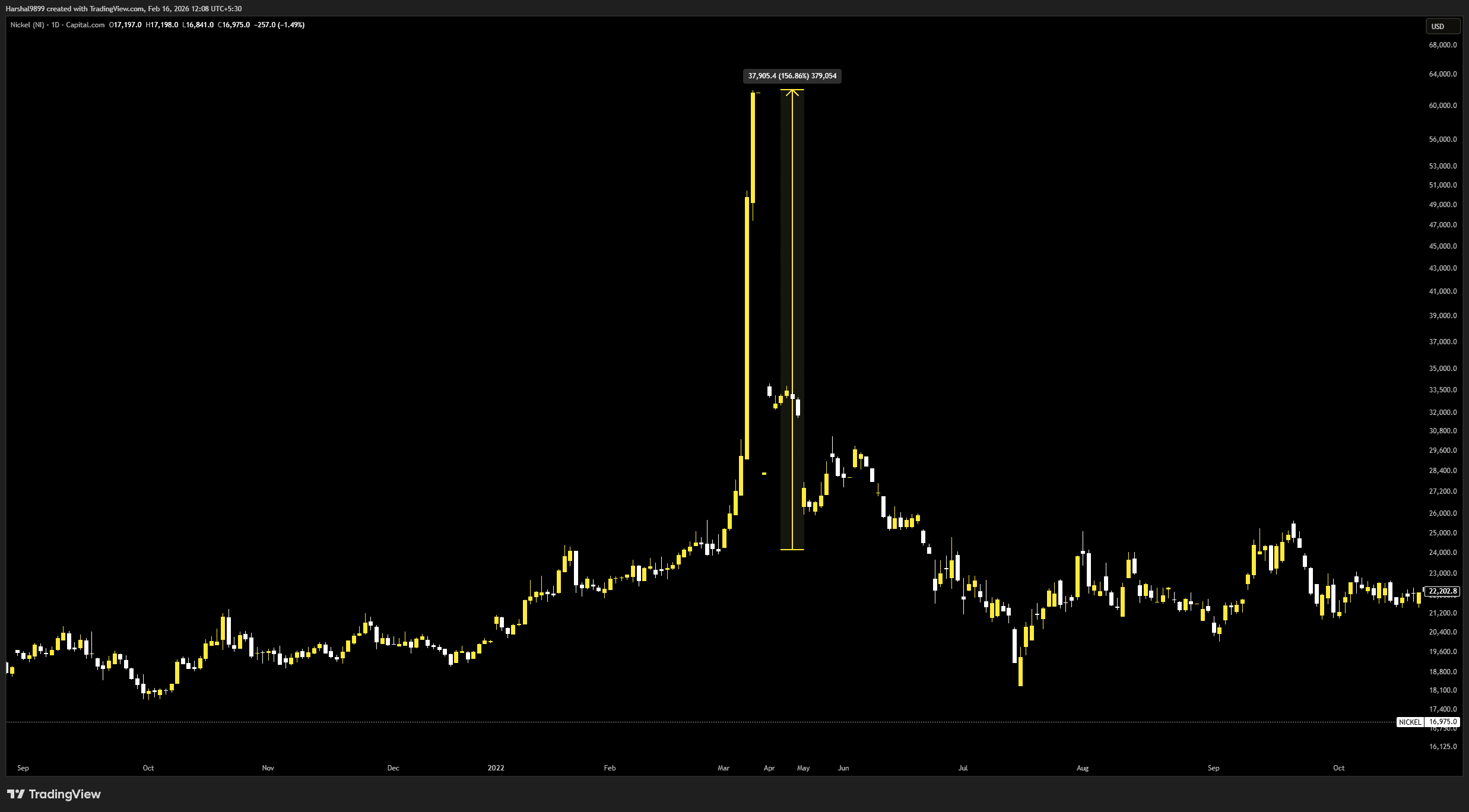

Within two trading sessions, nickel prices didn’t just rise—they detonated, briefly crossing levels above $100,000 per tonne.

This was not a rally. It was a squeeze.

Prices were no longer determined by industrial demand or supply expectations. They were determined by who needed to buy immediately to avoid default. And when the biggest participant is forced to buy into a rising market, price becomes a function of urgency, not value.

Act III — The Kill Switch

Faced with disorderly conditions, the London Metal Exchange halted trading.

Then came the most controversial decision: trades executed during the extreme spike were cancelled to restore market stability.

That moment changed how institutional investors view commodity exchanges.

Because exchanges promise price discovery.

But clearing systems promise stability.

When those promises collide, stability wins.

Act IV — The Lifeline

To prevent systemic damage, financing arrangements were assembled involving major global banks. Credit lines bought time. Positions were gradually stabilised. The market reopened days later, but the episode had already entered financial history.

What looked like a price spike from the outside was, in reality, a stress fracture inside the global commodity system.

What the Nickel Squeeze Revealed

Most people remember the headline: nickel went vertical.

The real lessons were structural.

1. Commodity markets are small but leveraged

Compared to global equities or bonds, many commodity derivatives markets are thin. When stress hits, that thinness becomes a vacuum—and vacuums create price gaps.

2. Positioning can overwhelm fundamentals

Nickel didn’t surge because demand suddenly exploded. It surged because positioning forced buying into an illiquid market.

3. Transparency matters

Large off-exchange exposures can amplify volatility when markets move sharply. When positions are bigger than liquidity, prices stop behaving smoothly.

Why It Still Matters Today

Nickel sits at the crossroads of two powerful forces:

- industrial demand from steel and infrastructure

- structural demand from electrification and batteries

That combination makes it strategically critical—and structurally sensitive.

Any market that combines:

- concentrated positions

- limited liquidity

- supply uncertainty

can recreate the same dynamics.

The nickel squeeze wasn’t an anomaly.

It was a template.

INVasset Perspective

The deepest lesson is not about nickel. It is about markets.

In leveraged systems, price does not move when fundamentals change.

Price moves when liquidity disappears.

Investors often focus on direction. Professionals focus on positioning.

Nickel’s spike showed that being fundamentally correct is not enough if the market structure turns against you. When leverage meets scarcity, prices can detach from logic faster than models can respond.

Final Word

The Nickel Squeeze was not just a commodity event.

It was a live demonstration of how modern financial systems behave under stress.

Liquidity vanished.

Leverage demanded cash.

Rules bent to preserve stability.

Nickel didn’t just spike.

It exposed the architecture of markets.

And once you’ve seen the architecture, you start recognising the pattern elsewhere.

Disclaimer:

This blog is for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any financial instrument. Views expressed are based on publicly available information and market understanding at the time of writing and are subject to change. Readers should consult their financial advisor before making any investment decisions. Investments in markets are subject to risk.